From development land, residential land to townhomes whatever you are looking for RPM has the ideal location for you.

From development land, residential land to townhomes whatever you are looking for RPM has the ideal location for you.

Development Land

Specialists in sourcing and selling development land for commercial and residential projects. Explore current and past opportunities.

Residential Land

Across Australia’s East coast RPM has the ideal land to suit your lifestyle and dream home, explore the projects RPM is proud to be partners in selling.

Townhomes

With townhouses to suit every lifestyle and budget, find your perfect home today.

Apartments

Inner city & coastal new apartment projects. Explore our projects to find your perfect location and style of living.

RPM offer a comprehensive suite of professional services at every stage of your property journey.

RPM offer a comprehensive suite of professional services at every stage of your property journey.

Pioneering new benchmarks in property intelligence, know-how, and data-driven insights, read the RPM Group's story.

Our Story

Since 1994, RPM has grown to become the industry-leader with an expanding national presence; offering a comprehensive suite of services

Our Team

The heart of our business are the people who make it thrive. Discover the passion and dedication of our national team.

Careers

Our team of property experts is truly unparalleled. See how you can join this exceptional group and shape your future with us.

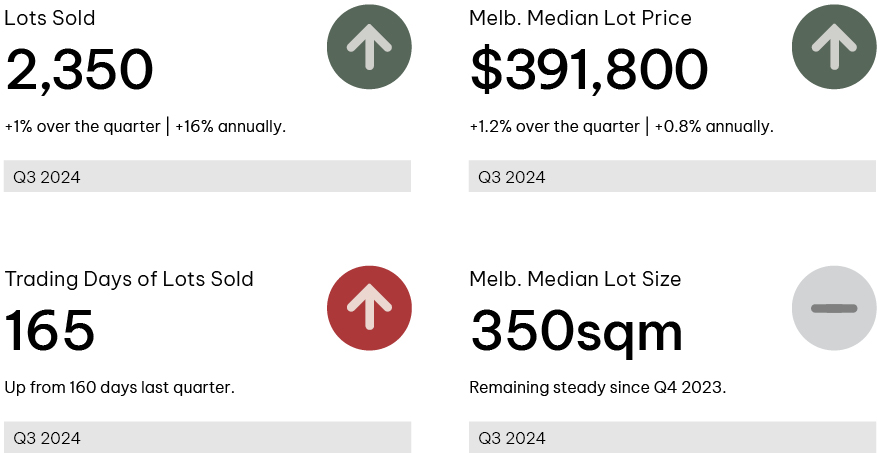

Sales activity across Melbourne and Geelong growth areas rose 1% in Q3, with2,350 lots sold. While this rise is slight, it signals a broader rebound in purchaser sentiment; this modest growth followed a July dip after a surge in June, driven by end-of-financial-year incentives.

Buyer sentiment improved as inflation concerns eased, with the annual CPI increase at 2.81% -the first time in over three years it fell within the Reserve Bank of Australia’s (RBA) 2%-3% target. International rate cuts and stage 3 tax adjustments in July also boosted disposable incomes, slightly enhancing borrowing capacity and buyer confidence.

September saw the strongest monthly sales activity since August 2022. Despite this, lot sales remain 38% below the ten-year monthly average, demonstrating that while confidence has improved, it remains measured.

Price sensitivity continues to be the biggest factor shaping buyer behaviour. Estates offering rebates and discounts (typically between 5% and 10% off the headline price) drove a significant portion of sales activity. New estates that are competitively priced to meet affordability needs also contributed significantly to sales. These pricing strategies have been especially effective for titled stock, which accounted for 41% of Q3 sales. As a result, headline prices saw a slight uptick. Melbourne’s median lot price increased by 1% both quarterly and annually, reaching $391,800, with the median lot size holding steady at 350sqm. The average time on market for lots increased slightly to around five and a half months.

New lot supply struggled in Q3, with releases dropping 4% to 1,746 lots. However, as stock returns stabilised at a little over 700 lots, the total stock on market rose slightly to 5,370 lots at the end of September.

This article references findings from our Q3 2024 Victoria Greenfield Market Report. Read the full report here.