From development land, residential land to townhomes whatever you are looking for RPM has the ideal location for you.

From development land, residential land to townhomes whatever you are looking for RPM has the ideal location for you.

Development Land

Specialists in sourcing and selling development land for commercial and residential projects. Explore current and past opportunities.

Residential Land

Across Australia’s East coast RPM has the ideal land to suit your lifestyle and dream home, explore the projects RPM is proud to be partners in selling.

Townhomes

With townhouses to suit every lifestyle and budget, find your perfect home today.

Apartments

Inner city & coastal new apartment projects. Explore our projects to find your perfect location and style of living.

RPM offer a comprehensive suite of professional services at every stage of your property journey.

RPM offer a comprehensive suite of professional services at every stage of your property journey.

Pioneering new benchmarks in property intelligence, know-how, and data-driven insights, read the RPM Group's story.

Our Story

Since 1994, RPM has grown to become the industry-leader with an expanding national presence; offering a comprehensive suite of services

Our Team

The heart of our business are the people who make it thrive. Discover the passion and dedication of our national team.

Careers

Our team of property experts is truly unparalleled. See how you can join this exceptional group and shape your future with us.

The north reclaimed its position as the most affordable of Melbourne’s four growth corridors, alongside the west, after losing the mantle at the end of 2023.

It also had the shortest period of average days on market in Q1 2024; at 143 days, this was higher than the previous quarter but in line with the time on market increasing across the board.

Our Q1 2024 Victoria Greenfield Market Report showed that sales surged 25% during Q1 with 666 lot sales and increases across all four sub-growth areas.

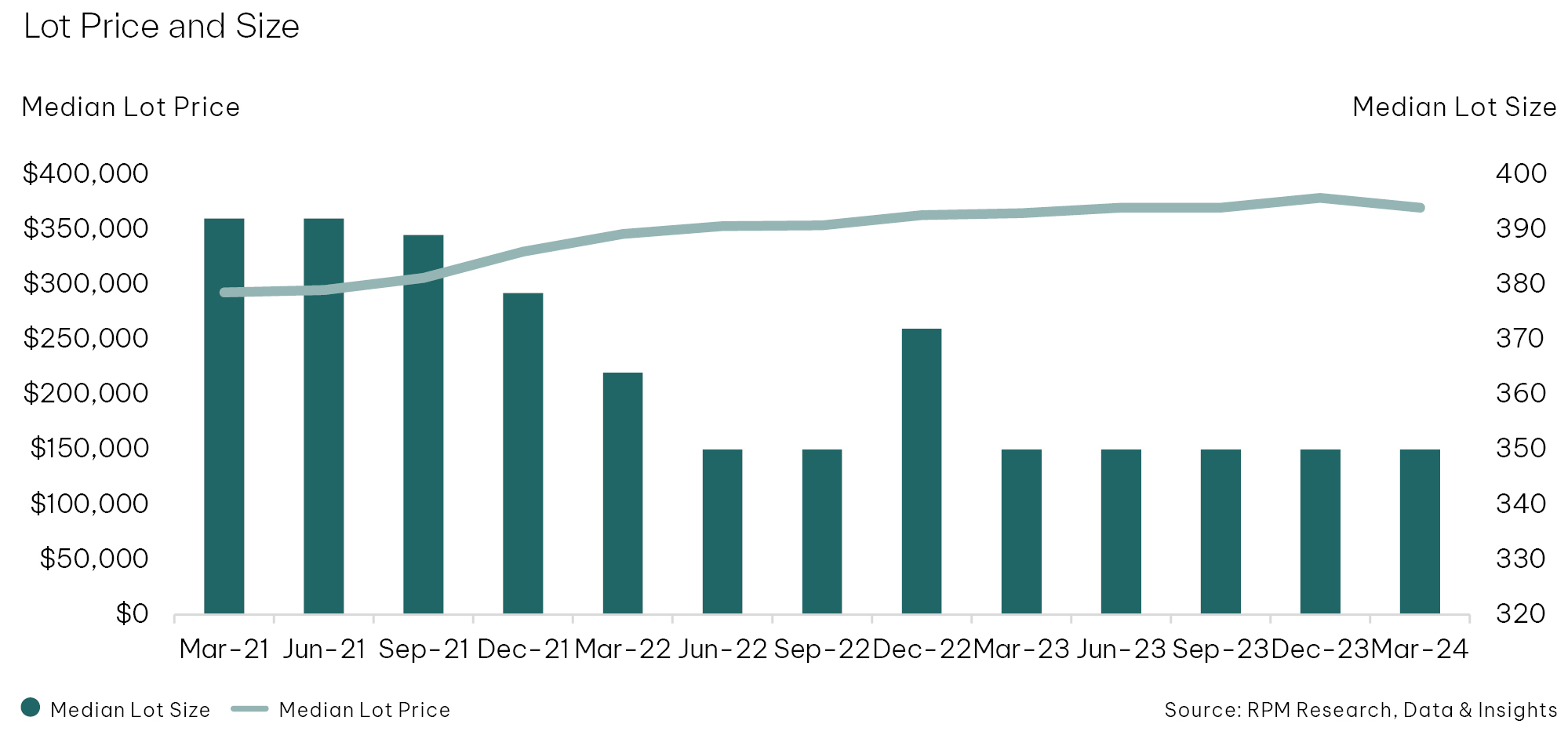

New supply in the north fell 11% to 454 lots while the median lot price also fell by 2.3% to $370,000 after rising 2.4% in Q4 2023.

This decline was observed in the subregions of Hume, Whittlesea and Sunbury, while Mitchell was the only subregion to see growth during the quarter.

The overall median lot size remained stable at 350sqm, although there continues to be a notable variation in lot sizes between Hume and Whittlesea compared to Sunbury and Mitchell.

RPM National Managing Director of Project Marketing Luke Kelly said the dip in the median sale price was driving increased demand in the northern corridor.

“The north claimed one in three sales across all growth corridors during Q1, showing its importance particularly to buyers looking for affordability,” he said.

“However, stock returns increased by 33% for the three months to March 31, which indicates that buyers are failing to reach settlement due to reduced borrowing capacity.”

“We are seeing improved buyer sentiment, but interest rates need to come down if we’re to see a dramatic improvement in the north’s fortunes.”

This article references findings from our Q1 2024 Victoria Greenfield Market Report.