From development land, residential land to townhomes whatever you are looking for RPM has the ideal location for you.

From development land, residential land to townhomes whatever you are looking for RPM has the ideal location for you.

Development Land

Specialists in sourcing and selling development land for commercial and residential projects. Explore current and past opportunities.

Residential Land

Across Australia’s East coast RPM has the ideal land to suit your lifestyle and dream home, explore the projects RPM is proud to be partners in selling.

Townhomes

With townhouses to suit every lifestyle and budget, find your perfect home today.

Apartments

Inner city & coastal new apartment projects. Explore our projects to find your perfect location and style of living.

RPM offer a comprehensive suite of professional services at every stage of your property journey.

RPM offer a comprehensive suite of professional services at every stage of your property journey.

Pioneering new benchmarks in property intelligence, know-how, and data-driven insights, read the RPM Group's story.

Our Story

Since 1994, RPM has grown to become the industry-leader with an expanding national presence; offering a comprehensive suite of services

Our Team

The heart of our business are the people who make it thrive. Discover the passion and dedication of our national team.

Careers

Our team of property experts is truly unparalleled. See how you can join this exceptional group and shape your future with us.

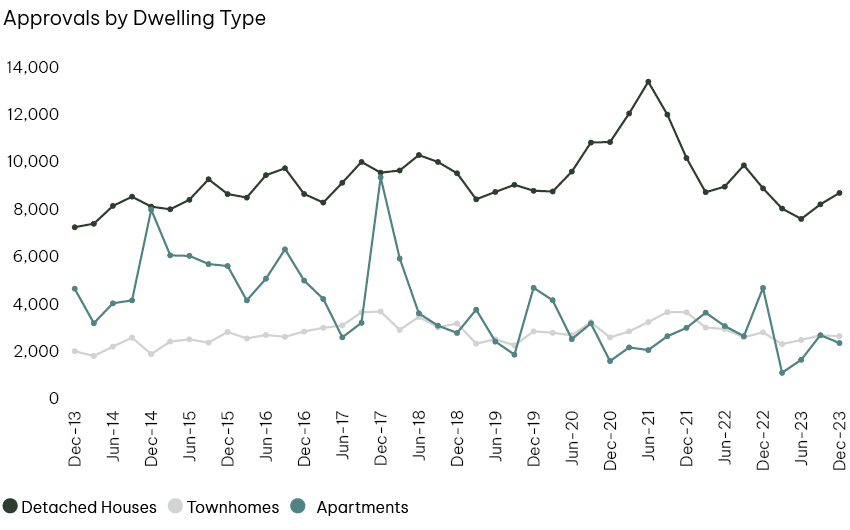

Our Q4 2023 Economic and Residential Property Market Report found that there have been notable declines in approvals and commencements for medium and higher-density dwellings – both of which are key components to the 70/30 plan.

The primary hindrance of building progress is labour costs. While raw material costs (or inputs) for building construction in Melbourne have remained relatively stable over the past year (a modest 1.3% increase in the year to Q4 2023), it was in stark contrast to the 14.2% increase recorded in the year to Q4 2022. This was helped by lower costs of early-stage construction materials including steel, timber, and cement, but balanced by increasing costs of late-stage construction goods such as electrical equipment.

However, outputs of ‘other building construction’ (the market price of completed townhomes and apartments) which take into account labour, material, plan, and subcontractor margins has seen a significant escalation. In Q4 alone, the index figure surged by 5.7%, marking the highest quarter-on-quarter increase since Q3 2010.

Over the course of CY23, Victoria’s townhome and apartment output index rose by 8.3%, surpassing the increases seen in New South Wales (+5.5%), Queensland (+6.1%), and the national average (+6.3%). This notable rise, despite relatively stable input costs, strongly suggests a continued upward trend in labour costs associated with townhome and apartment construction in Victoria.

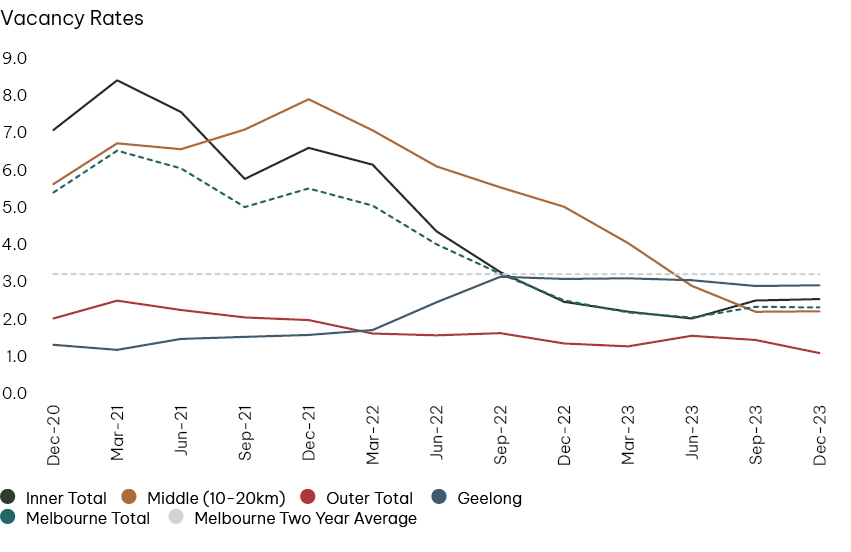

Furthermore, despite federal initiatives aimed at slowing the arrival of new migrants, January 2024 saw the highest level of long-term arrivals, as well as international student numbers largely recovering to 2019 levels are expected to exacerbate pressure on housing supply, which is already strained by low vacancy rates and a lack of significant planning reforms.

This article references findings from our Q4 2023 Economic and Residential Property Market Report.